Ezequiel Garcia-Lembergman

Assistant Professor at Pontificia Universidad Católica de Chile

I got my PhD in Economics at University of California, Berkeley in 2021.

My research interests are in international economics and macroeconomics. My CV is here, and a description of my research is here.

Contact me

-

Name:Ezequiel Garcia Lembergman

-

Email:

Fields

International Economics, Macroeconomics, Development Economics.

Research

Working papers

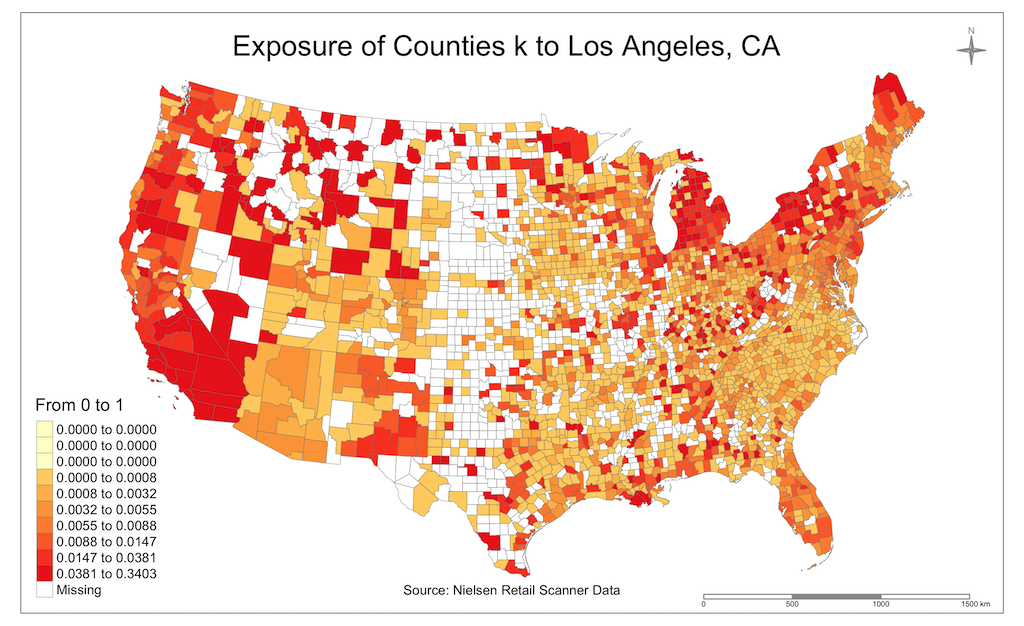

Multi-establishment Firms, Pricing and the Propagation of Local Shocks: Evidence from US Retail. Accepted, Review of Economics and Statistics

I study whether and how retail chains and their geographic distribution of stores contribute to the propagation of shocks across regions in the United States. Linking detailed store scanner micro-data to a county-level house price dataset for the period of the Great Recession, I investigate the spread of house-price induced local shocks through the networks of retail chains. My main empirical finding is that county-level prices are sensitive to shocks in distant counties that happen to be served by the same retail chains. A 10% drop in house prices in other counties that are served by the same retailers leads, on average, to a 1.4% decline in the local consumer retail price index. My results hold after conditioning on trade relationships due to geographic proximity. In fact, I document that once the retail chains' networks are controlled for, there is no additional role for propagation of shocks across nearby regions. Finally, while the network of retail chains is an important determinant of the effect local shocks have on consumer prices, it does not affect wages in distant regions, which suggests that the network of retail chains affects consumers' real income. I rationalize the reduced-form estimates in a model in which retail chains vary prices uniformly across their stores as a function of changes in market demand that they face at the (aggregate) chain level. I find that the calibrated model with uniform pricing can fully account for the reduced-form effects. Counterfactual analysis shows that uniform pricing and the geographic distribution of retail chains reduced cross-county dispersion in inflation by 40% during the Great Recession, benefiting consumers from low-income counties that were less exposed to drops in local house prices.

Importing After Exporting, with Facundo Albornoz. Revise and resubmit, Journal of European Economic Association.

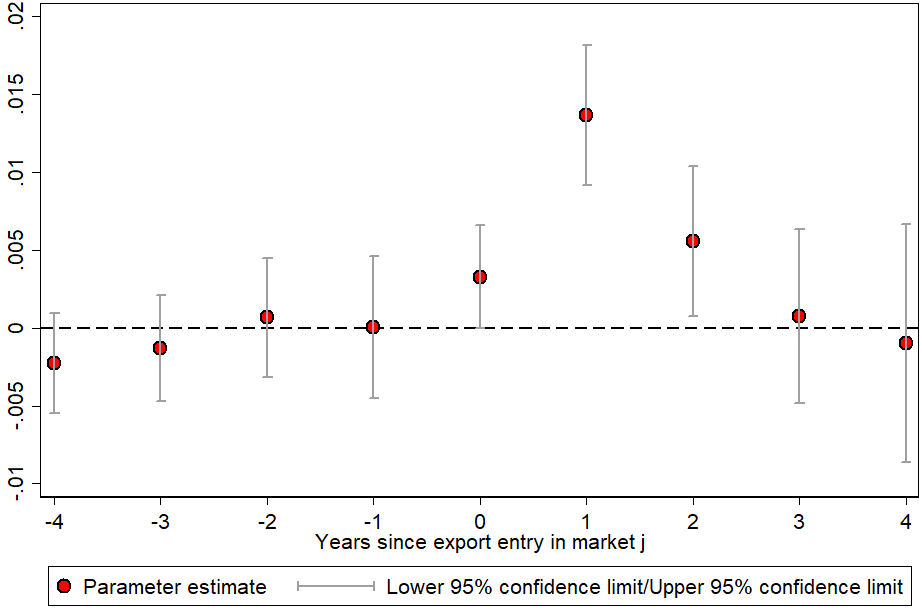

We uncover a novel fact about the relationship between exporting and importing. Using a comprehensive database of Argentine firms, we find that exporting to a new destination increases the probability of a firm beginning to import from that market within the lapse of one year. We develop a model of import and export decisions to study the effect of productivity and import costs on the intensive and extensive margins of importing. We show that "importing after exporting" implies that export entry reduces the cost of importing from that market. This effect is more likely to occur in distant markets, and in situations where importing involves non-homogeneous and rarely imported goods. Furthermore, new import activities from a new export destination continue regardless of whether the firm remains as an exporter in that market. This evidence is consistent with exporting reducing the information costs of importing. The effect of export entry on sourcing costs has implications that go beyond qualitative insights: according to our quantitative exercise, import costs fall 53% in a given destination after export entry, and the estimated import-cost savings increase for distant markets outside the Americas.

The Expectations of others, with Ina Hajdini, John Leer, Mathieu Pedemonte, and Raphael Schoenle. Revise and Resubmit, American Economic Journal: Macroeconomics.

Using a novel dataset that integrates inflation expectations with social networkconnections, we show that inflation expectations within one’s social network have a positive, causal relationship with individual inflation expectations. This relationship is stronger for groups that share commondemographic characteristics such as gender, income, or political affiliation and when salient information is shared. In a monetary-union New-Keynesian model, trade networks and socially determined inflation expectations induce imperfect risk-sharing, and can affect the inflation and real output propagation of local and aggregate shocks. To reduce welfare losses, monetary policy should optimally put more weight on the inflation rate of socially more connected regions.

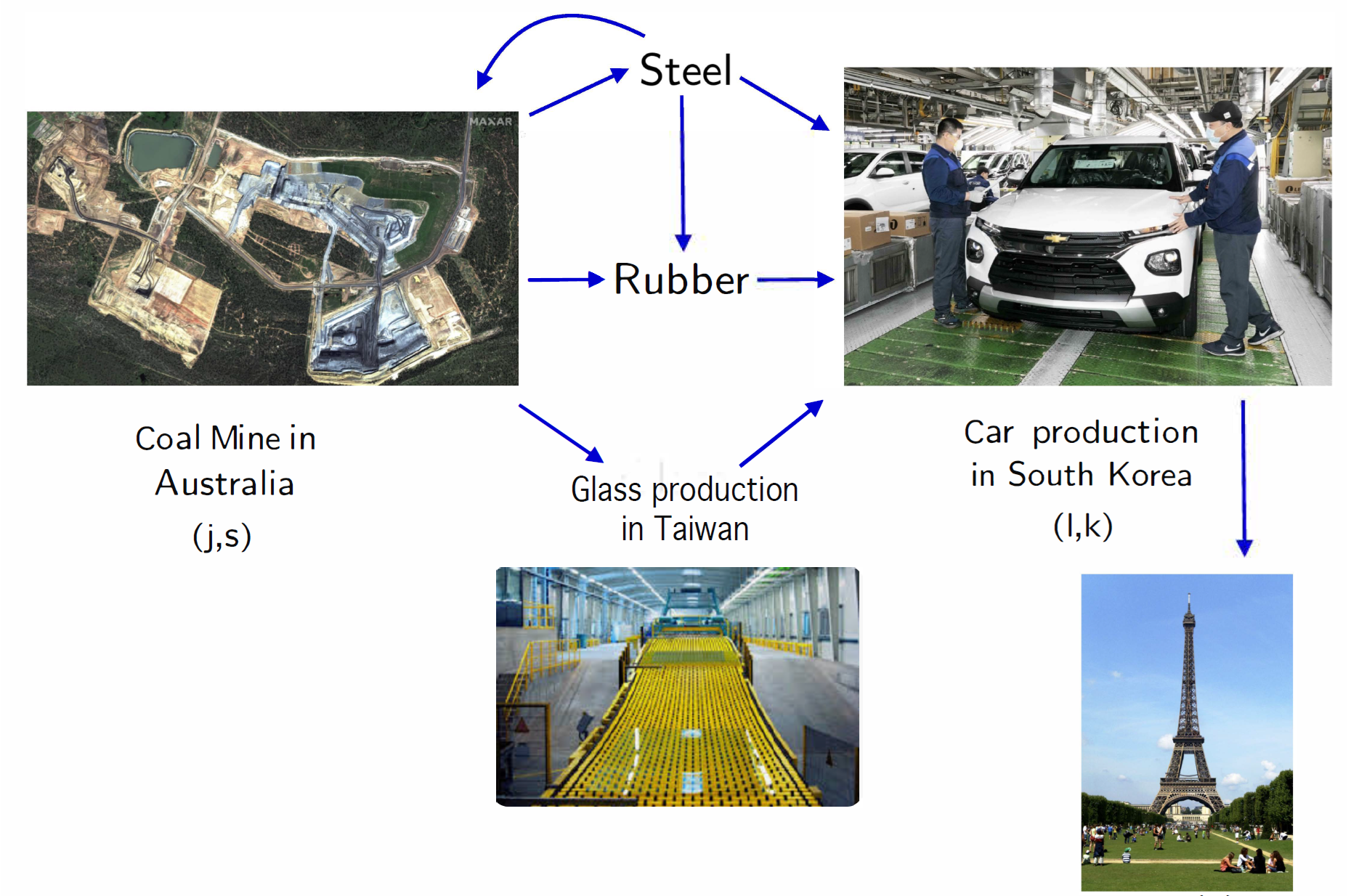

The Carbon Footprint of Multinational Production, with Natalia Ramondo, Andres Rodriguez-Clare, and Joseph Shapiro.

How does multinational production affect climate change? Global climate negotiations have set the goal of enormous transfers per year from rich to poor countries, including through private investment, to address climate change. Two stylized facts motivate the analysis of multinational production as a mechanism for such transfers. First, carbon emissions per dollar of value added or output differ substantially across countries, even conditional on industrial composition. Second, the emissions rate of a foreign-owned plant increases with the emission rate of its home country, suggesting that firms bring green technology with them when operating abroad. We develop and quantify a multi-country general equilibrium model of multinational production, trade, and energy to assess how policies encouraging multinational production would affect global carbon emissions and welfare.

Quantifying Emissions in the Global Economy, with Natalia Ramondo, Andres Rodriguez-Clare, and Joseph Shapiro.

We develop a quantitative trade model incorporating fossil fuel markets and carbon emissions. Using engineering estimates of mining extraction costs, we estimate the supply elasticity of fossil fuels and use the model to study how trade shocks and carbon taxes affect emissions, real income, and welfare. We consider three alternative Pigouvian taxes that differ only in the point of implementation: an extraction tax on fossil fuel mining, a production tax on the direct use of fossil fuels, and a consumption tax on the direct and indirect use of fossil fuels along global value chains. Global versions of the three taxes have similar global consequences and differ only via terms-of-trade effects; for example, fuel net exporters benefit more from global extraction taxes. For all three policies, a Pigouvian tax with the social cost of carbon equal to $100/ton decreases global emissions by 45% and real income by 0.6%, and increases global welfare 1.5%. We also characterize globally efficient unilateral taxes as a simple function of resulting leakage. The optimal unilateral production tax induces substantial leakage, motivating border adjustments. A unilateral consumption tax, with lower leakage, has a higher optimal tax level and welfare gain. Pairing a consumption and extraction tax outperforms either policy alone; for US or EU unilateral policy, this pairing increases global welfare gain by 40% relative to a consumption tax alone.

From Tax Amnesty to Bank Credit: The Transmission of Large-Scale Asset Repatriations through Firm-Bank Relationships , with Federico Bernini, Paula Donaldson, and Leticia Juarez.

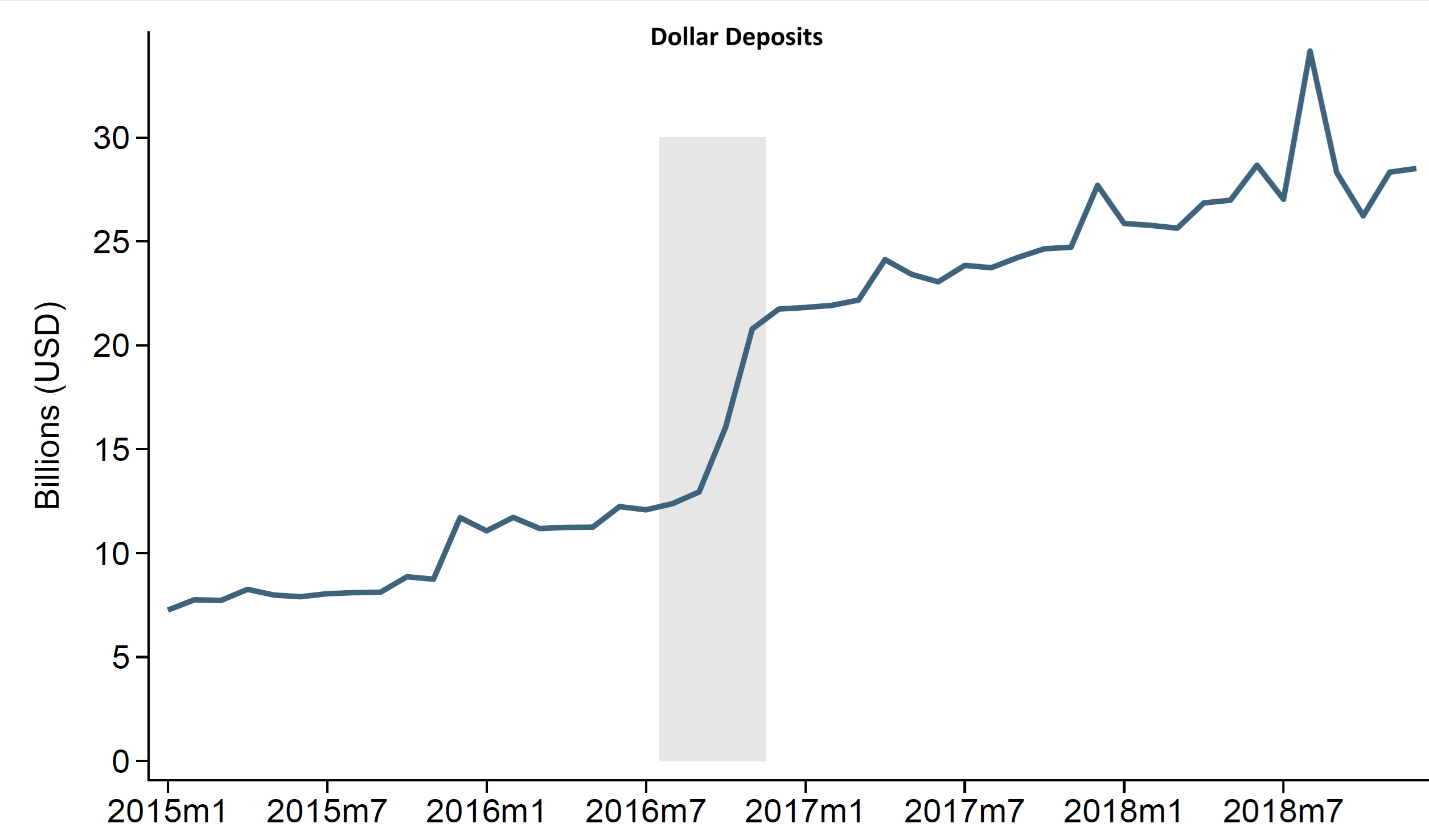

Over the past two decades, more than 40 countries have implemented tax amnesties to encourage the declaration and repatriation of previously hidden assets. While existing research primarily examines their direct fiscal effects, this paper highlights a novel channel: This policy has the potential to incentivize asset repatriations, expand the domestic financial sector and generate spillovers to private-sector firms. We study this mechanism in the context of Argentina’s 2016 Tax Amnesty which triggered a massive inflow of savings into domestic banks, predominantly in U.S. dollars, effectively doubling dollar-denominated deposits within a single quarter. These large-scale capital inflows provide a unique source of variation to examine how banks respond to foreign-currency liquidity shocks and how such shocks propagate to firms. Exploiting heterogeneity in banks’ and firms’ exposure to amnesty-related funds, we identify causal effects: banks with greater exposure significantly expanded lending, while connected firms increased borrowing, imports of intermediate inputs, exports, and employment. To interpret these findings and assess aggregate implications, we develop a general equilibrium model with heterogeneous banks and financial frictions. Counterfactual analysis indicates that the credit expansion induced by the tax amnesty raised GDP by 0.4 percent. Overall, our results show that tax amnesties can stimulate economic activity by deepening the financial sector, generating real effects beyond their direct impact on government revenue.

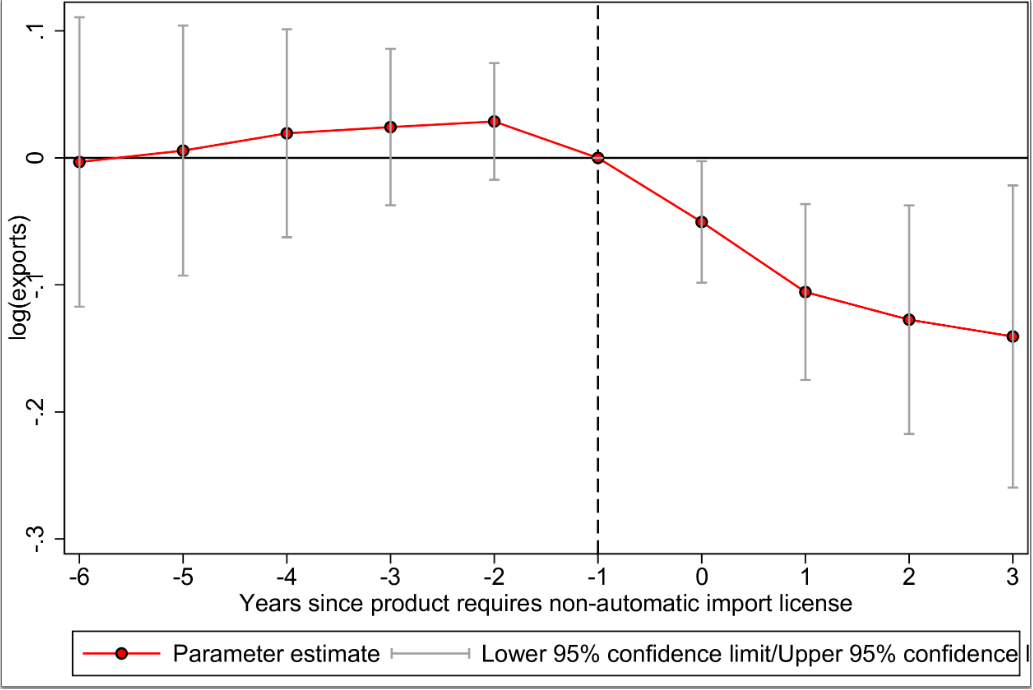

The Downstream Consequences of Non-Tariff Trade Barriers: Theory and Evidence from Import Licenses in Argentina , with Federico Bernini, and Leticia Juarez.

As WTO regulations rendered tariffs less viable, the trade policy landscape experienced a significant transformation: Non-tariff barriers have proliferated, becoming a central instrument of countries’ trade policy. How do Non-Tariff import Barriers affect downstream firms? What role do firm market power and market concentration play in shaping the effects of these barriers? This paper investigates the effects of import licenses (NAILs) in Argentina from 2005 to 2011. We construct a novel database with yearly data on products that require import licenses to analyze the causal effects of NAILs on firms’ imports, exports, and employment. Our empirical strategy leverages the staggered introduction of NAILs as a unique opportunity for causal identification. We find that NAILs significantly reduce firm imports, leading firms reliant on these imported inputs to decrease exports and employment. In a trade model with oligopolistic competition in export markets, we provide conditions under which firms’ market power can shape the aggregate impact of NAILs. In markets where a firm is relatively large, it can respond to NAILs by adjusting its markups while maintaining relatively stable prices and output. This reduces the overall impact on consumer prices in more concentrated markets.

Other Writing

VoxDevLit Review: Foreign Direct Investment and Development, with Stefania Garetto, Nina Pavnik, Natalia Ramondo, Vanessa Alviarez, Laura Boudreau, Evangelina Dardati, Jingting Fan, Farid Farrokhi, Grace Gu, Galina Hale, David Hemous, Nicola Limodio, Isabela Manelici, Nicolas Morales, Ralf Martin, Nitya Pandalai-Nayar, Heitor Pellegrina, Jose Vasquez, and Pierre Vezina.

Work in Progress

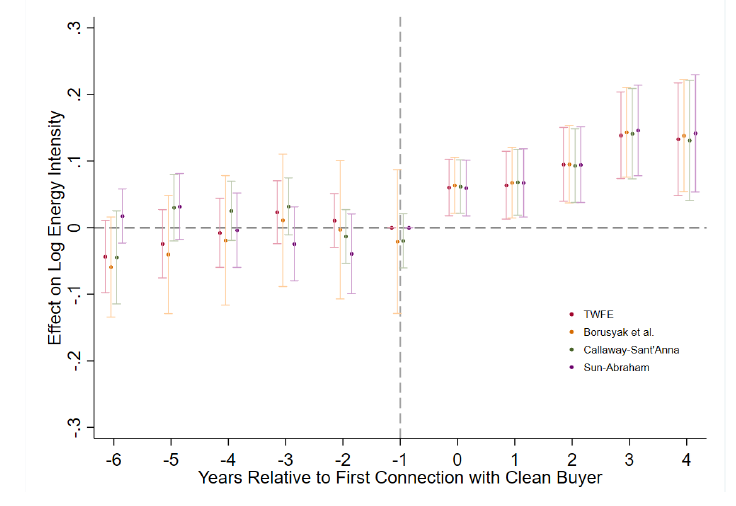

"Environmental Standards and Upstream Emissions: Evidence from Buyer–Supplier Links", with Leticia Juarez, Ignacio Marra, Christian Volpe

Firms increasingly adopt environmental standards, such as ISO certifications, to reduce emissions and promote sustainability. Yet it remains unclear how these private efforts affect their suppliers: do suppliers learn from cleaner buyers and adopt cleaner production practices, or do buyers that become cleaner shift dirtier production upstream? We combine detailed firm-to-firm transaction data with information on firm-level energy use and buyer ISO certifications for Uruguayan firms to examine the impact of joining an ISO-certified buyer supply chain on the $CO_2$ emissions of the supplier. We find that connecting to a clean buyer increases the energy share of total costs by 5 percent in subsequent years. These effects persist over time, consistent with sustained technological or process changes. Our results suggest that emissions reductions achieved by cleaner firms may be partially offset by increases along their supply chains.

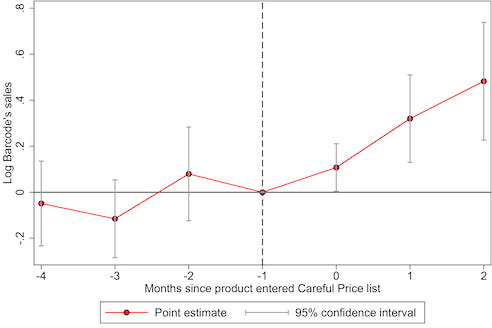

"Equilibrium Effects of Voluntary Price Control Policies", with Nano Barahona, Youssef Benzarti, Bernardo Diaz de Astarloa, Santiago Garriga, Diego Jimenez, Dario Tortarolo

This paper studies \textit{Precios Cuidados}, a voluntary program in Argentina where the government negotiated retail price caps with manufacturers in exchange for better shelf space and visibility in supermarkets. Using scanner data and a staggered difference-in-differences design, we find that the program lowered relative prices and increased sales of participating products compared with similar non-participating goods, without stockouts. The timing and size of the sales response suggest demand rose beyond the price effect. To interpret these results and measure welfare effects, we develop and estimate a model of firm pricing and consumer demand in which caps are negotiated between the government and firms. In the model, firms accept lower markups in return for marketing benefits. We show that price cap programs can raise consumer welfare by lowering the relative prices of regulated products and close substitutes while keeping firms willing to participate through marketing incentives.

Publications

The impact of export restrictions on production: A synthetic controls approach, with Martin Rossi & Rodolfo Stucchi. Journal of Latin American and Caribbean Economic Association, 2018.

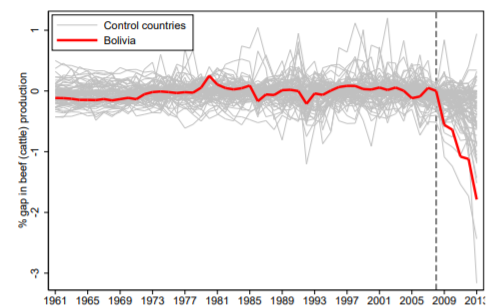

In spite of the generalized use of quantitative restrictions on exports, there is little empirical research on their effectiveness to achieve the intended effects of reducing exports, increasing production for domestic markets, and reducing domestic prices. This paper aims at filling this gap by estimating the impact of quantitative restrictions on cattle beef exports in Bolivia, applying a synthetic controls approach. Our main finding is that export restrictions have a negative impact not only on total production, but also on production for the domestic market. This fact, together with an increase in the domestic price, is consistent with a supply shift. The fact that export controls can shift supply and actually harm production for domestic markets bears important implications for the design of policies in the future.

Microeconomic dimensions of an export boom: Argentina, 2003-2011, with Facundo Albornoz and Leticia Juarez. The World Economy Journal, 2018.

This paper examines Argentine exports at the firm level between 2003 and 2011, a period of exceptional and sustained export growth. While at the product level, the pattern of specialization barely changed, exporters exhibit new dynamics in international markets: firms not only expanded sales abroad by increasing their exports in existing markets, but also by entering into new destinations and adding new products. That is, new export strategies allowed exporters achieve greater resistance to the variations in the macroeconomic environment. We find that the importance of the different export margins changes overtime: while the currency is depreciated, the intensive margin explains most of export growth, whereas the subextensive and extensive margins become the main source of export growth once the currency appreciates. We also uncover a strong complementarity between import and export growth.